Monexo is the best RBI Licensed P2P lending platform where people borrow and lend money to each other in India. Monexo provides an alternative investment and financing model which is 100% online, simple and fast. Borrowers get personal loans at attractive interest rates and flexible terms. Investors get to diversify their investment portfolio in a new asset class and earn monthly passive income.

Partner

Partner with Monexo to offer clients new investment options.

p2p investment: Peer-to-peer investing is becoming increasingly popular as it allows people to borrow directly from each other without involving any financial institutions. This provides certain advantages which are not available through traditional banking methods.

p2p platform: Peer-to-peer (P2P) services are gaining traction as they allow two individuals to directly interact, removing the need for a third party. It is a great option for those looking for an easy, secure and cost-effective way of exchanging data.

p2p finance: P2P lending is revolutionizing personal finance by allowing people to borrow and lend money directly from each other, without the need for a third-party such as a bank or other financial institution. This way of doing business is safer, faster and more efficient than traditional lending systems.

P2P marketplace: A peer-to-peer marketplace is a site that connects buyers and sellers together. It’s a great way to find the products or services you need while offering those you already have. This type of platform allows people to transact with each other on their own terms, helping them save time and money.

return on investment: Return on Investment (ROI) allows investors to gauge how much money they’ve either made or lost in comparison to the original amount of investment. It is a key performance metric essential for measuring the profitability and efficiency of investments.

credit score: An individual’s credit score is a numerical indication of their financial dependability, factoring in both their credit and spending histories. This rating gives lenders and creditors a better understanding of the person’s ability to make timely payments.

Lender: A lender offers funds to an individual or company, expecting them back with interest. This can come in the form of an individual, a public/private organization, or a financial institution.

Borrower: Borrowers are either individuals or organizations who take out loans from lenders and commit to paying them back within the agreed timeline.

Amplify Wealth

Using our interactive investment calculator, see how your money can compound and grow with Monexo

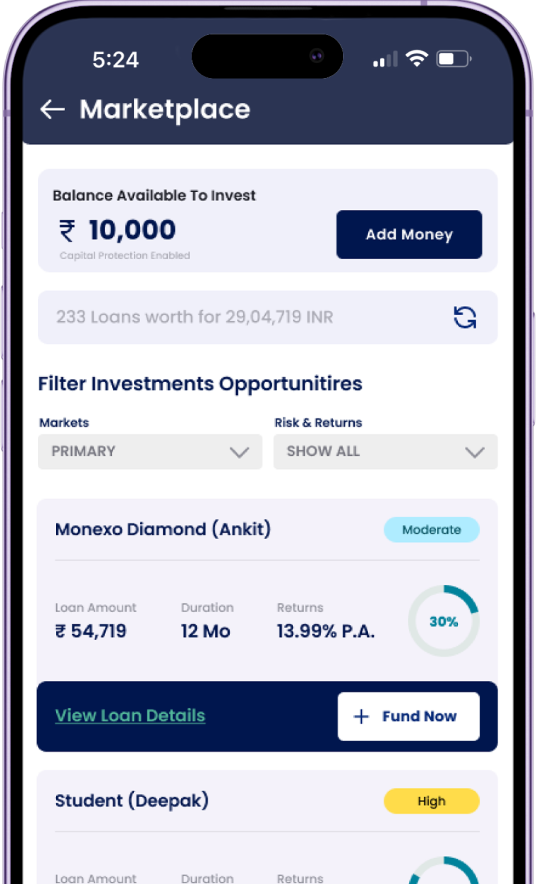

If you put your money in many different places, you can earn more money and lower your chances of losing money. Be smart when you choose where to put your money, and make sure you are in charge of all your investments.

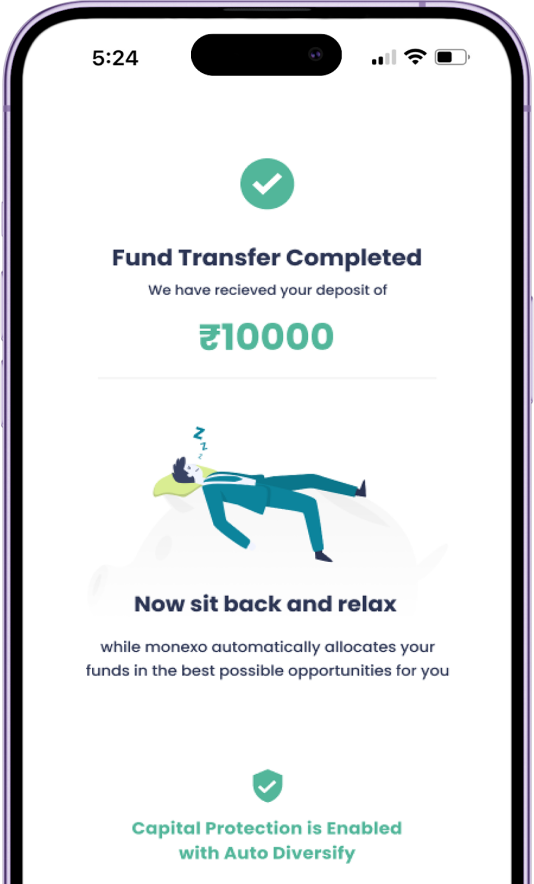

Investors can withdraw earnings at maturity, or even before.

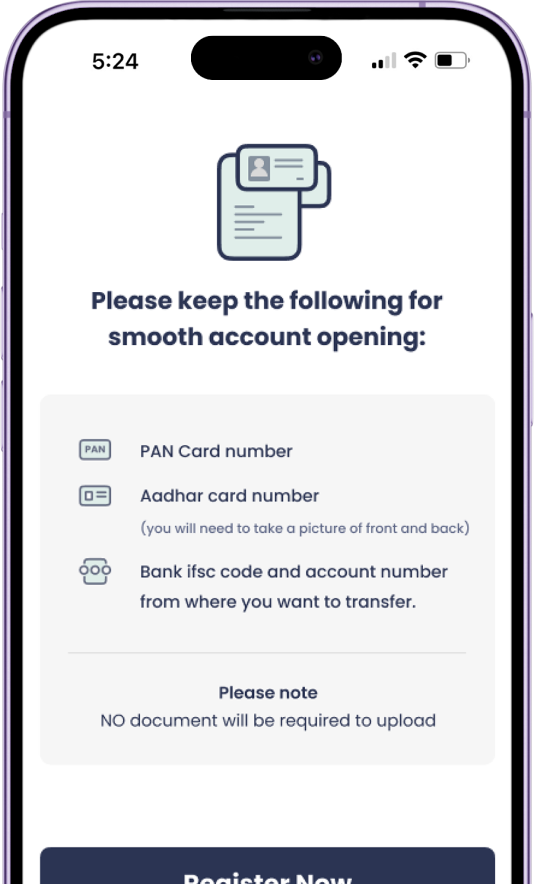

We will provide you with comprehensive information about each investment opportunity, including investment highlights, risks, terms, and potential earnings.

100%

Transparent

We prioritize investment safety, so we review every borrower's history and set appropriate interest rates accordingly.

Best

Interest Rates

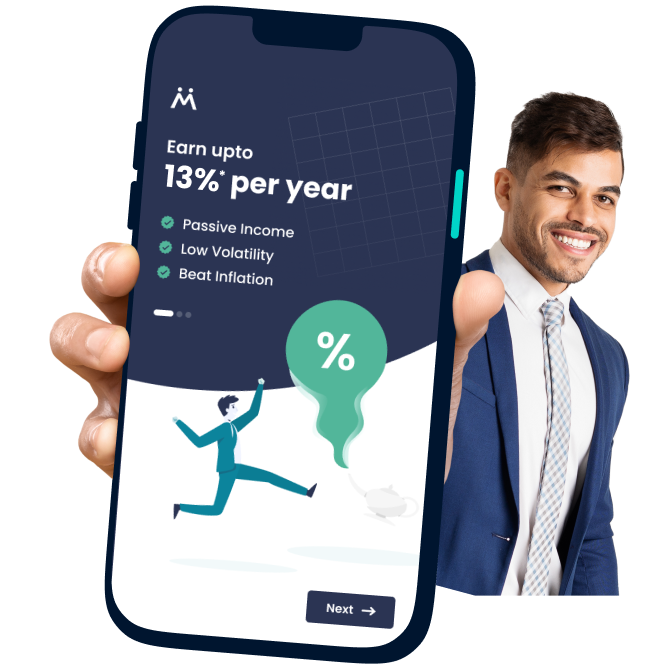

Earn high returns on your investments with regular payments and interest rates of 13-20%. Build wealth and passive income.

Wall of Happy Customers

Amit Bhise

Co Founder, PPC Corp

I really love how simple it is to invest via Monexo. It is truly a revolutionary P2P lending platform that has a clear understanding of the Indian context of borrowing and lending & risks related to that space. The team is really co-operative and they solve customer grievances on priority.

Rashmi Yadav

Co Founder, PPC Corp

Monexo is a great platform for people who want to invest their money in options other than FDs and the stock market. I really like how simple and transparent it is to invest via Monexo. Great job team!

Jeevan Goyal

Co Founder, PPC Corp

I found P2P lending at Monexo Grow is a great platform for people who want to invest a small amount and get good returns. The returns are much higher than FDs and the stock markets with way less volatility.

Ankit Roy

Co Founder, PPC Corp

There is a good site where people can give loans in a simple and transparent manner.it is an excellent platform for investors to get better returns on their money as compared to FDs and Stock market.

Rajiveer Pathak

Co Founder, PPC Corp

Investing with them was one of the best experiences, the staff members are very helpful and friendly, they provide you with the best option and take all precautions to ensure that your money is safe.

Rakshit Sarang

Co Founder, PPC Corp

For those looking for alternative investment options to FDs and the stock market, Monexo is a great platform. I really like how simple and transparent it is to invest via Monexo. Great job team!

Amit Bhise

Co Founder, PPC Corp

I really love how simple it is to invest via Monexo. It is truly a revolutionary P2P lending platform that has a clear understanding of the Indian context of borrowing and lending & risks related to that space. The team is really co-operative and they solve customer grievances on priority.

Rashmi Yadav

Co Founder, PPC Corp

Monexo is a great platform for people who want to invest their money in options other than FDs and the stock market. I really like how simple and transparent it is to invest via Monexo. Great job team!

Jeevan Goyal

Co Founder, PPC Corp

I found P2P lending at Monexo Grow is a great platform for people who want to invest a small amount and get good returns. The returns are much higher than FDs and the stock markets with way less volatility.

Ankit Roy

Co Founder, PPC Corp

There is a good site where people can give loans in a simple and transparent manner.it is an excellent platform for investors to get better returns on their money as compared to FDs and Stock market.

Rajiveer Pathak

Co Founder, PPC Corp

Investing with them was one of the best experiences, the staff members are very helpful and friendly, they provide you with the best option and take all precautions to ensure that your money is safe.

Rakshit Sarang

Co Founder, PPC Corp

For those looking for alternative investment options to FDs and the stock market, Monexo is a great platform. I really like how simple and transparent it is to invest via Monexo. Great job team!

Amit Bhise

Co Founder, PPC Corp

I really love how simple it is to invest via Monexo. It is truly a revolutionary P2P lending platform that has a clear understanding of the Indian context of borrowing and lending & risks related to that space. The team is really co-operative and they solve customer grievances on priority.

Rashmi Yadav

Co Founder, PPC Corp

Monexo is a great platform for people who want to invest their money in options other than FDs and the stock market. I really like how simple and transparent it is to invest via Monexo. Great job team!

Jeevan Goyal

Co Founder, PPC Corp

I found P2P lending at Monexo Grow is a great platform for people who want to invest a small amount and get good returns. The returns are much higher than FDs and the stock markets with way less volatility.

Ankit Roy

Co Founder, PPC Corp

There is a good site where people can give loans in a simple and transparent manner.it is an excellent platform for investors to get better returns on their money as compared to FDs and Stock market.

Rajiveer Pathak

Co Founder, PPC Corp

Investing with them was one of the best experiences, the staff members are very helpful and friendly, they provide you with the best option and take all precautions to ensure that your money is safe.

Rakshit Sarang

Co Founder, PPC Corp

For those looking for alternative investment options to FDs and the stock market, Monexo is a great platform. I really like how simple and transparent it is to invest via Monexo. Great job team!

Amit Bhise

Co Founder, PPC Corp

I really love how simple it is to invest via Monexo. It is truly a revolutionary P2P lending platform that has a clear understanding of the Indian context of borrowing and lending & risks related to that space. The team is really co-operative and they solve customer grievances on priority.

Rashmi Yadav

Co Founder, PPC Corp

Monexo is a great platform for people who want to invest their money in options other than FDs and the stock market. I really like how simple and transparent it is to invest via Monexo. Great job team!

Jeevan Goyal

Co Founder, PPC Corp

I found P2P lending at Monexo Grow is a great platform for people who want to invest a small amount and get good returns. The returns are much higher than FDs and the stock markets with way less volatility.

Ankit Roy

Co Founder, PPC Corp

There is a good site where people can give loans in a simple and transparent manner.it is an excellent platform for investors to get better returns on their money as compared to FDs and Stock market.

Rajiveer Pathak

Co Founder, PPC Corp

Investing with them was one of the best experiences, the staff members are very helpful and friendly, they provide you with the best option and take all precautions to ensure that your money is safe.

Rakshit Sarang

Co Founder, PPC Corp

For those looking for alternative investment options to FDs and the stock market, Monexo is a great platform. I really like how simple and transparent it is to invest via Monexo. Great job team!